Regional Sustainability ›› 2023, Vol. 4 ›› Issue (3): 235-248.doi: 10.1016/j.regsus.2023.07.001cstr: 32279.14.j.regsus.2023.07.001

• Full Length Article • Previous Articles Next Articles

Md. Mominur RAHMAN*( )

)

Received:2023-02-02

Revised:2023-04-08

Accepted:2023-07-26

Published:2023-09-30

Online:2023-10-20

Contact:

*E-mail address: Md. Mominur RAHMAN. Impact of taxes on the 2030 Agenda for Sustainable Development: Evidence from Organization for Economic Co-operation and Development (OECD) countries[J]. Regional Sustainability, 2023, 4(3): 235-248.

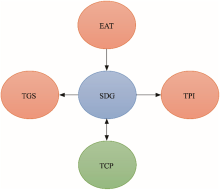

Fig. 1.

Conceptual research model constructed in this study. H1, there is an association between EAT and SDGs; H2, there is a relationship between TPI and SDGs; H3, there is a link between TCP and SDGs; H4, there is a connection between TGS and SDGs."

Table 1

Variable description and data sources."

| Variable | Measurement | Data sources |

|---|---|---|

| Sustainable Development Goals (SDGs) | The SDGs are global indices that measure progress toward achieving the United Nations’ SDGs. SDGs provide a scorecard for each country on the 17 SDGs based on variables that measure the country's progress toward achieving each goal. The variable is designed to help countries identify areas where they need to focus their efforts to achieve SDGs and to track progress over time. | Sustainable Development Report ( |

| Effective average tax (EAT) | EAT indicates the percentage of total taxable amount over all taxes of OECD countries from 2000 to 2021. | Heimberger ( |

| Tax on personal income (TPI) | TPI is measured in the percentage of taxes on net income and individual capital gain over the total taxes of OECD countries from 2000 to 2021. | OECD ( |

| Tax on corporate profits (TCP) | TCP is measured in the percentage of taxes on company's net profit and capital gains over the total taxes of OECD countries from 2000 to 2021. | OECD ( |

| Tax on goods and services (TGS) | TGS is measured in the percentage of taxes on goods and services over the total taxes of OECD countries from 2000 to 2021. | OECD ( |

Table 2

Descriptive statistics of five variables (SDGs, EAT, TPI, TCP, and TGS)."

| Variable | Mean | Median | Minimum | Maximum | Standard deviation | Skewness | Kurtosis |

|---|---|---|---|---|---|---|---|

| SDGs | 0.783 | 0.735 | 0.515 | 0.921 | 0.340 | 0.289 | 3.101 |

| EAT | 0.373 | 0.329 | 0.168 | 0.433 | 0.218 | 0.427 | 9.615 |

| TPI | 0.129 | 0.118 | 0.109 | 0.225 | 0.055 | 0.217 | 4.853 |

| TCP | 0.559 | 0.575 | 0.667 | 0.177 | 0.311 | 0.122 | 3.946 |

| TGS | 0.613 | 0.695 | 0.235 | 0.791 | 0.245 | 0.229 | 7.844 |

Table 3

Correlation matrix of five variables (SDGs, EAT, TPI, TCP, and TGS)."

| Variable | SDGs | EAT | TPI | TCP | TGS |

|---|---|---|---|---|---|

| SDGs | 1.000 | ||||

| EAT | 0.439** (10.011) | 1.000 | |||

| TPI | 0.321* (4.173) | 0.072* (5.287) | 1.000 | ||

| TCP | 0.468* (6.048) | 0.113** (3.386) | 0.101** (4.271) | 1.000 | |

| TGS | 0.293* (5.763) | 0.055* (2.873) | 0.003* (3.762) | 0.138* (4.278) | 1.000 |

Fig. 2.

Technique route of econometric modeling used in this study."

Table 5

Results of second-generation panel unit root tests (Cross-sectional Augmented Dickey-Fuller (CADF) test and Cross-sectional Im, Pesaran, and Shin (CIPS) test) for five variables (SDGs, EAT, TPI, TCP, and TGS)."

| Variable | CIPS | CADF | ||

|---|---|---|---|---|

| I(0) | I(1) | I(0) | I(1) | |

| SDGs | 2.142 | 5.062* | 1.912 | 4.168** |

| EAT | 1.480 | 3.195* | 1.325 | 2.941* |

| TPI | 2.151 | 3.910** | 2.039* | 3.020** |

| TCP | 2.104 | 4.932* | 2.179 | 4.020* |

| TGS | 1.991 | 4.565** | 2.592* | 3.841* |

Table 6

Result of panel cointegration test with four test statistics based on the Error Correction Model, including the parameters of Ga, Gt, Pa, and Pt."

| Statistics | Gt | Ga | Pt | Pa |

|---|---|---|---|---|

| Value | 3.464** | 9.294* | 8.286* | 9.704*** |

| Z-value | 3.431 | 1.719 | 1.472 | 0.135 |

| P-value | 0.006 | 0.050 | 0.051 | 0.090 |

| Robust P-value | 0.004 | 0.000 | 0.000 | 0.000 |

Table 7

Result of long-run estimation test with augmented mean group (AMG) and Common Correlated Effects Mean Group (CCEMG)."

| Variable | AMG | CCEMG | ||

|---|---|---|---|---|

| Coefficient | P-value | Coefficient | P-value | |

| Constant | 2.235** | 0.000 | 3.597 | 0.307 |

| EAT | 0.399* | 0.042 | 0.500** | 0.006 |

| TPI | 0.204* | 0.030 | 0.309*** | 0.060 |

| TCP | 0.545** | 0.001 | 0.568** | 0.000 |

| TGS | 0.559** | 0.000 | 0.671** | 0.000 |

| RMSE | 0.018 | 0.020 | ||

Table 8

Results of the Dumitrescu-Hurlin (DH) test of five variables (SDG, EAT, TPI, TCP, and TGS)."

| Null hypothesis (H0) | W-value | Z-value | P-value | Remark |

|---|---|---|---|---|

| EAT$\nLeftrightarrow$SDGs | 4.146** | 3.485 | 0.001 | EAT→SDGs |

| SDGs$\nLeftrightarrow$EAT | 5.861 | 5.082 | 0.271 | |

| TPI$\nLeftrightarrow$SDGs | 6.701** | 5.571 | 0.000 | TPI→SDGs |

| SDGs$\nLeftrightarrow$TPI | 4.760 | 3.648 | 0.443 | |

| TCP$\nLeftrightarrow$SDGs | 4.254** | 3.398 | 0.009 | TCP↔SDGs |

| SDGs$\nLeftrightarrow$TCP | 2.576** | 0.854 | 0.000 | |

| TGS$\nLeftrightarrow$SDGs | 4.145** | 3.359 | 0.002 | TGS→SDGs |

| SDGs$\nLeftrightarrow$TGS | 3.673 | 1.738 | 0.384 |

Fig. 3.

Causality relationship of SDGs with EAT, TPI, TCP, and TGS. The one-way arrow indicates a unidirectional causal relationship; the two-way arrow indicates a bi-directional causal relationship."

| [1] | Adegboye A., Erin O., Asongu S., 2022. Taxing Africa for Inclusive Human Development: The Mediating Role of Governance Quality. [2023-04-08]. https://mpra.ub.uni-muenchen.de/111753/1/MPRA_paper_111753.pdf. |

| [2] |

Alavuotunki K., Haapanen M., Pirttilä J., 2019. The effects of the value-added tax on revenue and inequality. J. Dev. Stud. 55(4), 490-508.

doi: 10.1080/00220388.2017.1400015 |

| [3] |

Angelopoulos K., Economides G., Kammas P., 2007. Tax-spending policies and economic growth: Theoretical predictions and evidence from the OECD. Eur. J. Polit. Econ. 23(4), 885-902.

doi: 10.1016/j.ejpoleco.2006.10.001 |

| [4] | Anguelov N., 2017. Lowering the marginal corporate tax rate: Why the debate? Econ. Affa. 37(2), 213-228. |

| [5] |

Artiach T., Lee D., Nelson D., et al., 2010. The determinants of corporate sustainability performance. Account. Finance. 50(1), 31-51.

doi: 10.1111/acfi.2010.50.issue-1 |

| [6] |

Asmah E.E., Kwaw A.F., Titriku E., 2020. Trade misinvoicing effects on tax revenue in sub-Saharan Africa: The role of tax holidays and regulatory quality. Ann. Public Coop. Econ. 91(4), 649-672.

doi: 10.1111/apce.v91.4 |

| [7] | Barrios S., d’Andria D., Gesualdo M., 2020. Reducing tax compliance costs through corporate tax base harmonization in the European Union. J. Int. Account. Audit. Tax. 41, doi: 10.1016/j.intaccaudtax.2020.100355. |

| [8] |

Bartik T.J., 1992. The effects of state and local taxes on economic development: A review of recent research. Econ. Dev. Q. 6(1), 102-111.

doi: 10.1177/089124249200600110 |

| [9] | Bird R.M., 2013. Taxation and Development: What Have We Learned from Fifty Years of Research? [2023-04-08]. https://opendocs.ids.ac.uk/opendocs/bitstream/handle/20.500.12413/11255/ICTD_RiB_1_2.11.pdf?sequence=1&isAllowed=y. |

| [10] | Bird R.M., Martinez-Vazquez J., 2014. Taxation and Development:The Weakest Link? Essays in Honor of Roy Bahl. Cheltenham: Edward Elgar Publishing, 1-102. |

| [11] |

Bird R., Davis-Nozemack K., 2018. Tax avoidance as a sustainability problem. J. Bus. Ethics. 151(4), 1009-1025.

doi: 10.1007/s10551-016-3162-2 |

| [12] | Bond S., Eberhardt M., 2013. Accounting for Unobserved Heterogeneity in Panel Time Series Models. [2023-04-08]. https://lezme.github.io/markuseberhardt/BEMC.pdf. |

| [13] |

Castro G.Á., Camarillo D.B.R., 2014. Determinants of tax revenue in OECD countries over the period 2001-2011. Contaduría y Administración. 59(3), 35-59.

doi: 10.1016/S0186-1042(14)71265-3 |

| [14] | Chan K.H., Lo Agnes W.Y., Mo Phylls L.L., 2015. An empirical analysis of the changes in tax audit focus on international transfer pricing. J. Int. Account. Audit. Tax. 24, 94-104. |

| [15] | Chou C.P., Bentler P.M., 1990. Model modification in covariance structure modeling: A comparison among Likelihood Ratio, Lagrange Multiplier, and Wald Tests. Multivariate Behav. Res. 25(1), 115-136. |

| [16] |

Danish, Zhang, J.W., Hassan, S.T., et al., 2020. Toward achieving environmental sustainability target in Organization for Economic Co-operation and Development countries: The role of real income, research and development, and transport infrastructure. Sustain. Dev. 28(1), 83-90.

doi: 10.1002/sd.1973 |

| [17] | de Paepe G., Dickinson B., 2014. Tax Revenues as a Motor for Sustainable Development. Development Co-operation Report. [2023-04-08]. https://www.oecd-ilibrary.org/development/development-co-operation-report-2014/tax-revenues-as-a-motor-for-sustainable-development_dcr-2014-11-en. |

| [18] | Deb B.C., Rahman M.M., Rahman M.S., 2022. The impact of environmental management accounting on environmental and financial performance: Empirical evidence from Bangladesh. J. Account. Organ. Change. 19(3), 420-446. |

| [19] |

Diaz-Sarachaga J.M., Jato-Espino D., Castro-Fresno D., 2018. Is the Sustainable Development Goals (SDG) index an adequate framework to measure the progress of the 2030 Agenda? Sustain. Dev. 26(6), 663-671.

doi: 10.1002/sd.v26.6 |

| [20] |

Dumitrescu E.I., Hurlin C., 2012. Testing for Granger non-causality in heterogeneous panels. Econ. Model. 29(4), 1450-1460.

doi: 10.1016/j.econmod.2012.02.014 |

| [21] |

Faghri A., 2023. Climate change and urban transport sustainability. Curr. Urban Stud. 11(1), 60-71.

doi: 10.4236/cus.2023.111004 |

| [22] | Fernando Y., Chukai C., 2018. Value co-creation, goods and service tax (GST) impacts on sustainable logistic performance. Res. Transp. Bus. Manag. 28, 92-102. |

| [23] | Gechert S., Heimberger P., 2022. Do corporate tax cuts boost economic growth? Eur. Econ. Rev. 147, 104157, doi: 10.1016/j.euroecorev.2022.104157. |

| [24] |

Goss E.P., Phillips J.M., 1999. Do business tax incentives contribute to a divergence in economic growth? Econ. Dev. Q. 13(3), 217-228.

doi: 10.1177/089124249901300302 |

| [25] |

Hadri K., Kurozumi E., 2012. A simple panel stationarity test in the presence of serial correlation and a common factor. Econ. Lett. 115(1), 31-34.

doi: 10.1016/j.econlet.2011.11.036 |

| [26] | Heimberger P., 2021. Corporate tax competition: A meta-analysis. Eur. J. Political Econ. 69, doi: 10.1016/j.ejpoleco.2021.102002. |

| [27] | Hulten C.R., Robertson J.W., 1985. Corporate tax policy and economic growth:An analysis of the 1981 and 1982 tax acts. In: Dogramaci, A., Adam, N.R., (eds.). Managerial Issues in Productivity Analysis. Berlin: Springer, 5-48. |

| [28] |

Jarboui A., Kachouri M., Riguen R., 2020. Tax avoidance: Do board gender diversity and sustainability performance make a difference? Journal of Financial Crime. 27(4), 1389-1408.

doi: 10.1108/JFC-09-2019-0122 |

| [29] | Kaldor N., 1963. Taxation for economic development. J. Mod. Afr. 1(1), 7-23. |

| [30] | Kaldor N., 1965. The role of taxation in economic development. In: Robinson, E.A.G., (ed.). Problems in Economic Development:Proceedings of a Conference held by the International Economic Association. London: Palgrave Macmillan, 170-195. |

| [31] | Kalkuhl M., Fernandez B.M., Schwerhoff G., et al., 2018. Can land taxes foster sustainable development? An assessment of fiscal, distributional and implementation issues. Land Use Pol. 78, 338-352. |

| [32] |

Kanbur R., Paukkeri T., Pirttilä J., et al., 2018. Optimal taxation and public provision for poverty reduction. Int. Tax Public Finance. 25(1), 64-98.

doi: 10.1007/s10797-017-9443-6 |

| [33] |

Kouam J.C., Asongu S.A., 2022. Effects of taxation on social innovation and implications for achieving sustainable development goals in developing countries: A literature review. Int. J. Innov. Stud. 6(4), 259-275.

doi: 10.1016/j.ijis.2022.08.002 |

| [34] |

Lee Y., Gordon R.H., 2005. Tax structure and economic growth. J. Public Econ. 89(5), 1027-1043.

doi: 10.1016/j.jpubeco.2004.07.002 |

| [35] | Marques M., Pinho C., Montenegro T.M., 2019. The effect of international income shifting on the link between real investment and corporate taxation. J. Int. Account. Audit. Tax. 36, 100268, doi: 10.1016/j.intaccaudtax.2019.100268. |

| [36] | Martinez-Vazquez J., Bird R.M., 2014. Sustainable development requires a good tax system. In: Bird, R.M., Martinez-Vazquez, J., (eds.). Taxation and Development:The Weakest Link? Cheltenham: Edward Elgar Publishing, 1-23. |

| [37] | Mathieu-Bolh N., 2017. Can tax reforms help achieve sustainable development? Resour Energy Econ. 50, 135-163. |

| [38] |

McGill G., 2010. The effects of taxation on sustainable development. Local Econ. 25(3), 251-263.

doi: 10.1080/02690941003784333 |

| [39] | Mirrlees J.A., 1986. The theory of optimal taxation. In: Arrow K.J., Intriligator, M.D., (eds.). Handbook of Mathematical Economics. Amsterdam: Elsevier, 1197-1249. |

| [40] | Mosquera-Valderrama I.J., 2019. Tax incentives:From an investment, tax, and sustainable development perspective. In: Chaisse, J., Choukroune, L., Jusoh, S., (eds.). Handbook of International Investment Law and Policy. Singapore: Springer, 1-21. |

| [41] |

Myles G.D., 2000. Taxation and Economic Growth. Fisc. Stud. 21(1), 141-168.

doi: 10.1111/fisc.2000.21.issue-1 |

| [42] |

Nellen A., Miles M., 2007. Taxes and Sustainability. J. Green Build. 2(4), 57-72.

doi: 10.3992/1943-4618 |

| [43] | Nerudová D., Hampel D., Janová J., et al., 2019. Tax system sustainability evaluation: A model for EU countries. Inter Econ. 54(3), 138-141. |

| [44] |

Neupane D., Adhikari P., Bhattarai D., et al., 2022. Does climate change affect the yield of the top three cereals and food security in the world? Earth. 3(1), 45-71.

doi: 10.3390/earth3010004 |

| [45] | OECD (Organization for Economic Co-operation and Development), 2022. OECD Tax Database. [2022-04-08]. https://www.oecd.org/tax/tax-policy/tax-database. |

| [46] |

Padovano F., Galli E., 2001. Tax rates and economic growth in the OECD countries. Econ. Inq. 39(1), 44-57.

doi: 10.1111/j.1465-7295.2001.tb00049.x |

| [47] | Peterson T., Bair Z., 2022. United States tax rates and economic growth. SAGE Open. 12(3), 1-13. |

| [48] | Rahman M.M., Rahman M.S., Deb B.C., 2021. Impact of corporate governance on tax management: Evidence from DSE listed banks. Bangladesh Economia. 1(1), 18-32. |

| [49] | Rahman M.M., 2022. The effect of taxation on sustainable development goals: evidence from emerging countries. Heliyon. 8(9), doi: 10.1016/j.heliyon.2022.e10512. |

| [50] | Rahman M.M., Halim M.A., 2022. Does the export-to-import ratio affect environmental sustainability? Evidence from BRICS countries. Energy Environ. doi: 10.1177/0958305X221134946. |

| [51] | Rahman M.S., Hasan M.J., Rahman M.M., 2020. Nexus between corporate tax rate and employment growth: Empirical evidence from Bangladesh. The Cost and Management. 48(5), 15-23. |

| [52] | Sachs J., Kroll C., Lafortune G., et al., 2021. Sustainable Development Report 2021. Cambridge: Cambridge University Press. |

| [53] | Samour A., Shahzad U., Mentel G., 2022. Moving toward sustainable development: Assessing the impacts of taxation and banking development on renewable energy in the UAE. Renew. Energ. 200, 706-713. |

| [54] | Sandmo A., 1975. Optimal taxation in the presence of externalities. The Swedish Journal of Economics. 86-98. |

| [55] |

Saqib N., 2022. Green energy, non-renewable energy, financial development and economic growth with carbon footprint: heterogeneous panel evidence from cross-country. Economic Research-Ekonomska Istraživanja. 35(3), 1-20.

doi: 10.1080/1331677X.2020.1845968 |

| [56] |

Sarafidis V., Wansbeek T., 2012. Cross-sectional dependence in panel data analysis. Econom. Rev. 31(5), 483-531.

doi: 10.1080/07474938.2011.611458 |

| [57] |

Simionescu M., Albu L.L., 2016. The impact of standard value added tax on economic growth in CEE-5 countries: econometric analysis and simulations. Technol. Econ. Dev. Econ. 22(6), 850-866.

doi: 10.3846/20294913.2016.1244710 |

| [58] | Sørensen P.B., 2007. The theory of optimal taxation: what is the policy relevance? Int. Tax Public Financ. 14, 383-406. |

| [59] | Usman M., Jahanger A., Makhdum M.S.A., et al., 2022. How do financial development, energy consumption, natural resources, and globalization affect Arctic countries’ economic growth and environmental quality? An advanced panel data simulation. Energy. 241, 122515, doi: 10.1016/j.energy.2021.122515. |

| [60] | Walker B., 2019. Facilitating SDGs by Tax System Reform. In: Walker, J., Pekmezovic, A., Walker, G., (eds.). Sustainable Development Goals: Harnessing Business to Achieve the SDGs through Finance, Technology, and Law Reform. New York: John Wiley & Sons Ltd. |

| [61] |

Wang X., Khurshid A., Qayyum S., et al., 2022. The role of green innovations, environmental policies and carbon taxes in achieving the sustainable development goals of carbon neutrality. Environ. Sci. Pollut. Res. 29(6), 8393-8407.

doi: 10.1007/s11356-021-16208-z |

| [62] | Wasylenko M., 2019. Taxation and Economic Development: The State of the Economic Literature. London: Taylor and Francis, 309-328. |

| [63] | World Bank, 2019. Taxation and the Sustainable Development Goals. [2022-04-08]. https://documents.worldbank.org/en/publication/documents-reports/documentdetail/860581538762337418/taxation-and-the-sustainable-development-goals-conference-report. |

| [64] |

Weller C.E., 2007. The benefits of progressive taxation in economic development. Rev. Radical. Polit. Econ. 39(3), 368-376.

doi: 10.1177/0486613407305286 |

| [65] |

Westerlund J., Edgerton D.L., 2007. A panel bootstrap cointegration test. Econ. Lett. 97(3), 185-190.

doi: 10.1016/j.econlet.2007.03.003 |

| [66] |

Yang J., Chen M.L., Fu C.Y., et al., 2020. Environmental policy, tax, and the target of sustainable development. Environ. Sci. Pollut. Res. 27(12), 12889-12898.

doi: 10.1007/s11356-019-05191-1 |

| [67] |

Yassine N., 2020. A sustainable economic production model: effects of quality and emissions tax from transportation. Ann. Oper. Res. 290(1), 73-94.

doi: 10.1007/s10479-018-3069-7 |

| [68] | Zhang Y.J., Song Y., 2022. Tax rebates, technological innovation and sustainable development: Evidence from Chinese micro-level data. Technol. Forecast. Soc. Change. 176, 121481, doi: 10.1016/j.techfore.2022.121481. |

| [1] | LIU Binsheng, ZHANG Xiaohui, TIAN Junfeng, CAO Ruimin, SUN Xinzhang, XUE Bin. Rural sustainable development: A case study of the Zaozhuang Innovation Demonstration Zone in China [J]. Regional Sustainability, 2023, 4(4): 390-404. |

| [2] | Surendra Singh JATAV, Kalu NAIK. Measuring the agricultural sustainability of India: An application of Pressure-State-Response (PSR) model [J]. Regional Sustainability, 2023, 4(3): 218-234. |

| [3] | Firoz AHMAD, Nazimur Rahman TALUKDAR, Laxmi GOPARAJU, Chandrashekhar BIRADAR, Shiv Kumar DHYANI, Javed RIZVI. GIS-based assessment of land-agroforestry potentiality of Jharkhand State, India [J]. Regional Sustainability, 2022, 3(3): 254-268. |

| [4] | Giribabu DANDABATHULA, Sudhakar Reddy CHINTALA, Sonali GHOSH, Padmapriya BALAKRISHNAN, Chandra Shekhar JHA. Exploring the nexus between Indian forestry and the Sustainable Development Goals [J]. Regional Sustainability, 2021, 2(4): 308-323. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

REGSUS Wechat

REGSUS Wechat

新公网安备 65010402001202号

新公网安备 65010402001202号